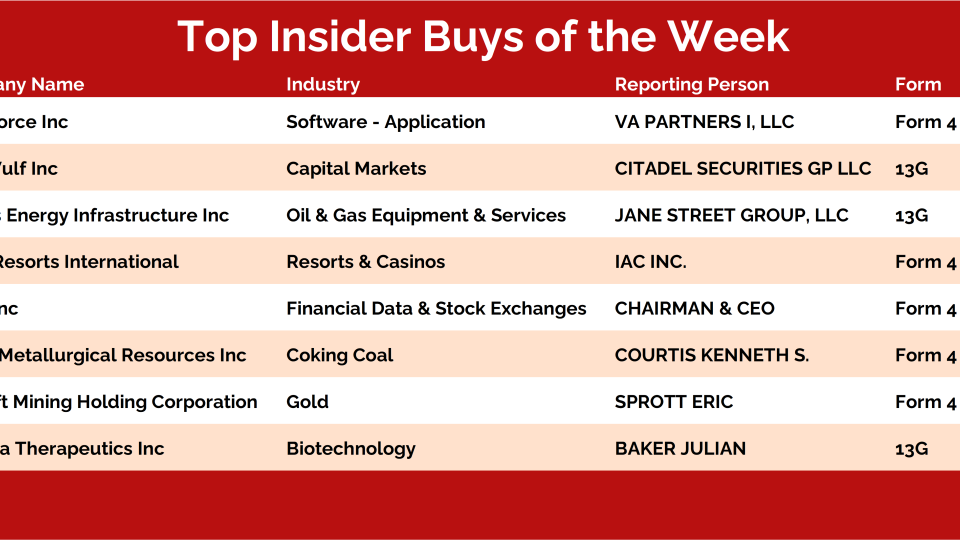

Every weekend, I dig into our insider activity tracker looking for the biggest conviction buys — and this week checked all the boxes: Baker Bros, coal stocks, big software bets, and precious metals.

I'm filing today's trade under the category of "Hard Trades." Not because it's particularly hard to execute or because it's a complicated multi-legged spread. It won't require an excessive amount of...

Dividend Aristocrats are easily some of the most desirable investments on Wall Street. These are the names that have increased dividends for at least 25 years, providing steadily increasing income to...