The first section dives deep into the US Stock Market, and the second half covers International Stock Markets and FICC (Fixed Income, Commodities & Currencies).

As a trader, I've always looked forward to Mondays. These days, I like them even more because I get to act upon some great trading ideas published in the Under the Hood report which...

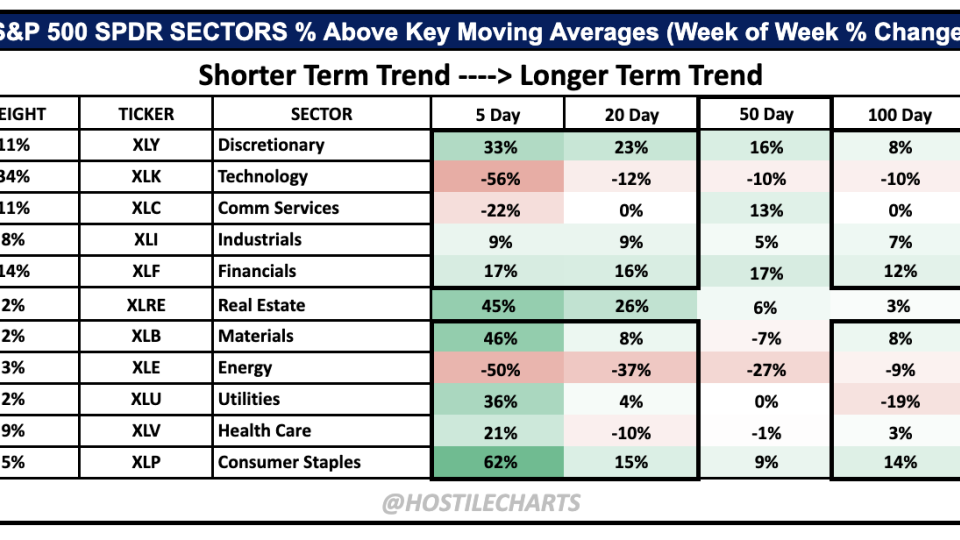

We retired our "Five Bull Market Barometers" in mid-July to make room for a new weekly post that's focused on the three most important charts for the week ahead...

Energy stocks in India, the US, and other global markets have been a disaster for a long time. In fact, despite strength in stocks as an asset class, we've been finding short opportunities in the sector.

Dividend aristocrats are easily some of the most desirable investments on Wall Street. These are the names that have increased dividends for at least 25 years, providing steadily increasing...

The All Star Charts research team is about to release a new report called the "Young Aristocrats." I've seen the preview and one of the stocks on their list is setting up nicely today for a breakout, so I'm wasting no time to get involved.

You're probably hearing a lot about SPACs these days. SPAC technically stands for "Special-Purpose Acquisition Company. So in this video I chat with Howard about these "Blank Check" vehicles. Historically they haven't exactly had the greatest...

After 33 months of zero progress, the market is proving that it is finally time for Transportation stocks to move forward. We call these big bases. It was a well-deserved consolidation in prices after a historic run throughout 2016-2017.

Something we've been working on internally this year is using various bottoms-up tools and scans to complement our top-down approach. One way we’re doing...