I know this might be breaking news to some of you, but there are often great opportunities to be had in international stocks. And the All Star Charts International...

The largest insider transaction on today’s list is a Form 4 filing by two members of the Starbucks $SBUX board of directors, chair Mellody Hobson and member Richard Allison.

They reported purchases of SBUX worth a combined $5.9 million.

This is the weekly post that aggregates all the charts we put together throughout the week and organizes them all into one, easy to flip through deck....

Our International Hall of Famers list is composed of the 100 largest US-listed international stocks, or ADRs. We’ve also sprinkled in some of the largest ADRs from countries that did not make the...

This week’s upside surprise in inflation is raising the stakes for next week’s FOMC meeting. While the 10-year T-Note yield is still just below its June peak, yields at the shorter-end of the curve...

Every week, the team publishes the Follow The Flow report which surfaces unusual options activity. This is a report I reference often, not because I want to do the same trades that surface in the...

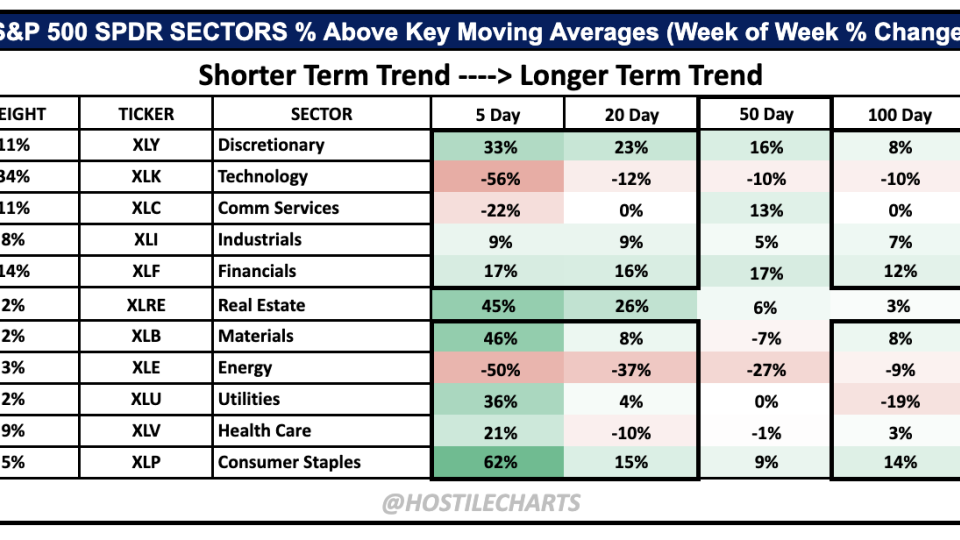

Although volatility has returned to equity markets this week, we continue to see pockets of strength in a variety of areas and individual stocks from our Inside Scoop universe.