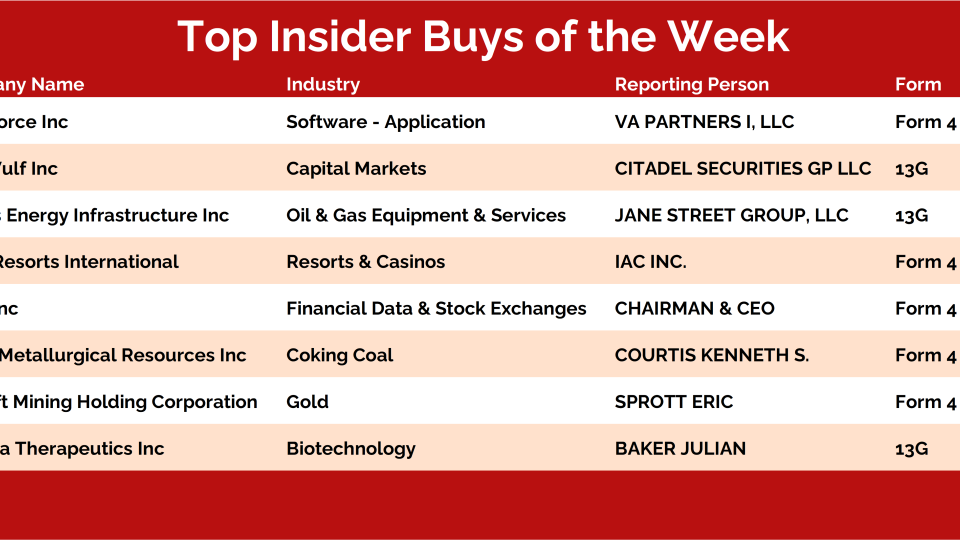

Every weekend, I dig into our insider activity tracker looking for the biggest conviction buys — and this week checked all the boxes: Baker Bros, coal stocks, big software bets, and precious metals.

I'm about to show you what a healthy chart off the bear market lows looks like. One of the beautiful things about this chart is it's not heavily reliant on any one company.

This is a sector ETF for a corner of the stock market we believe...

{kind=link}

{kind=link}