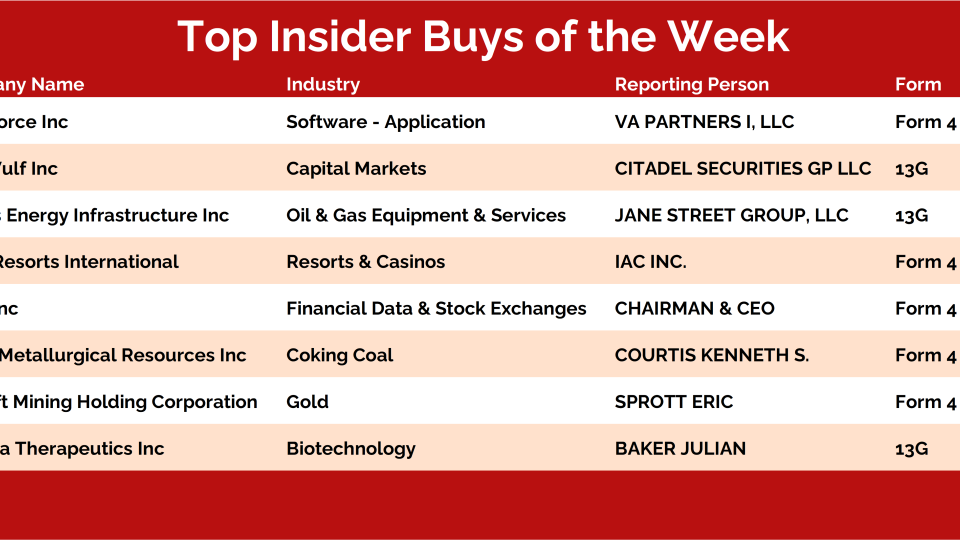

Every weekend, I dig into our insider activity tracker looking for the biggest conviction buys — and this week checked all the boxes: Baker Bros, coal stocks, big software bets, and precious metals.

HMI Capital Management just made a bold move, raising its stake in nCino Inc $NCNO and making the Wilmington, North Carolina-based fintech outfit its No. 2 holding.

Escape velocity is defined as the minimum speed that is required for an object to free itself from the gravitational force exerted by a massive object.

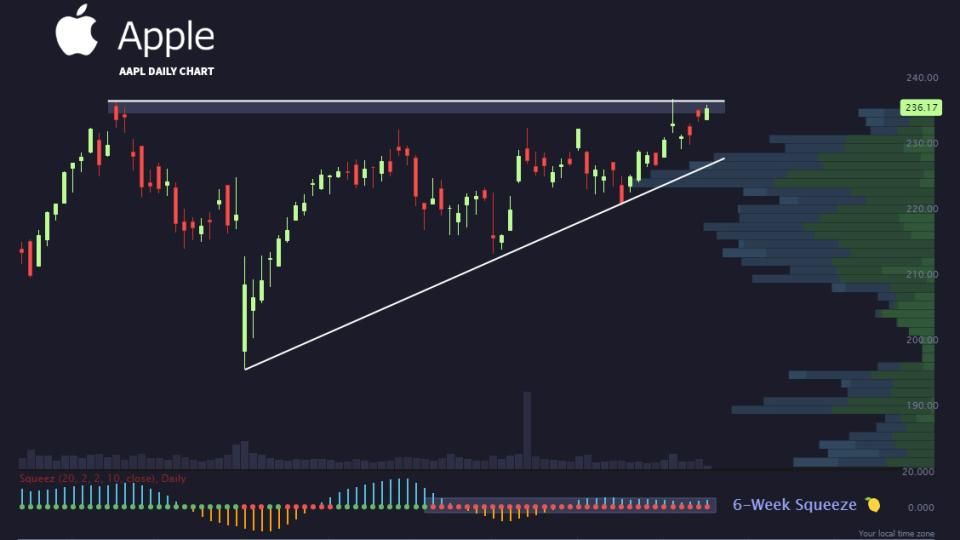

I can't think of a better image to describe Bitcoin; after months of chopsolidation, the...