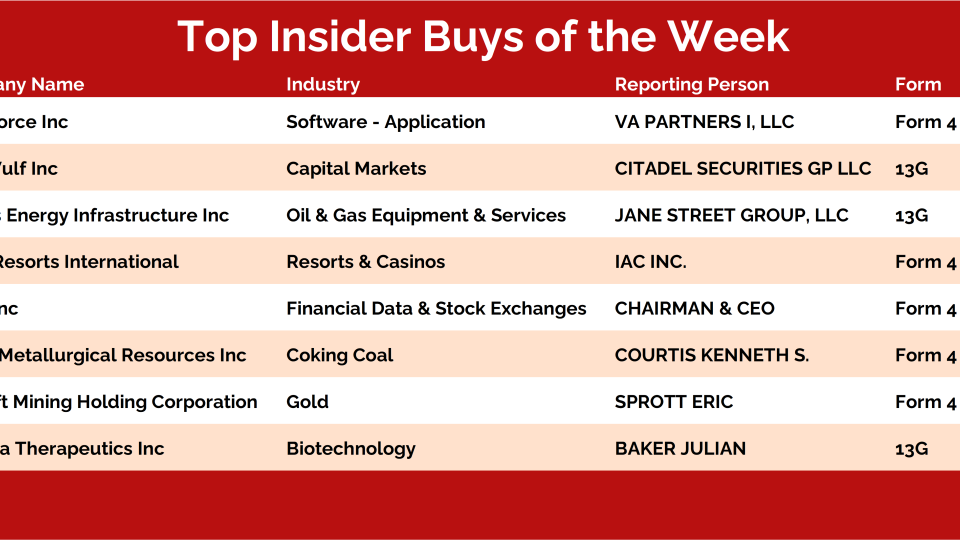

Every weekend, I dig into our insider activity tracker looking for the biggest conviction buys — and this week checked all the boxes: Baker Bros, coal stocks, big software bets, and precious metals.

What I try to do at the start of the year is to not allow my bias cloud my judgment. I try to stay focused on price and let the market guide me. I'm not...

This is the weekly post that aggregates all the charts we put together throughout the week and organizes them all into one, easy to flip through deck....

Here is a list of trade ideas organized by date, ticker symbol and directional bias. Please make sure you have clicked on the link and read the details surrounding the trade before acting upon any of them. Also, make sure you have checked with your...

Perhaps 2022 marks the worst on record, or at least the past 100 years. Nevertheless, we’ve all witnessed extraordinary selling pressure in what has...

The largest insider transaction on today’s list comes in a Form 4 filing by director Roxanne Austin, who revealed a $2 million purchase in CrowdStrike Holdings $CRWD.

CRWD is trading at its lowest level in years as it looks to find support at...