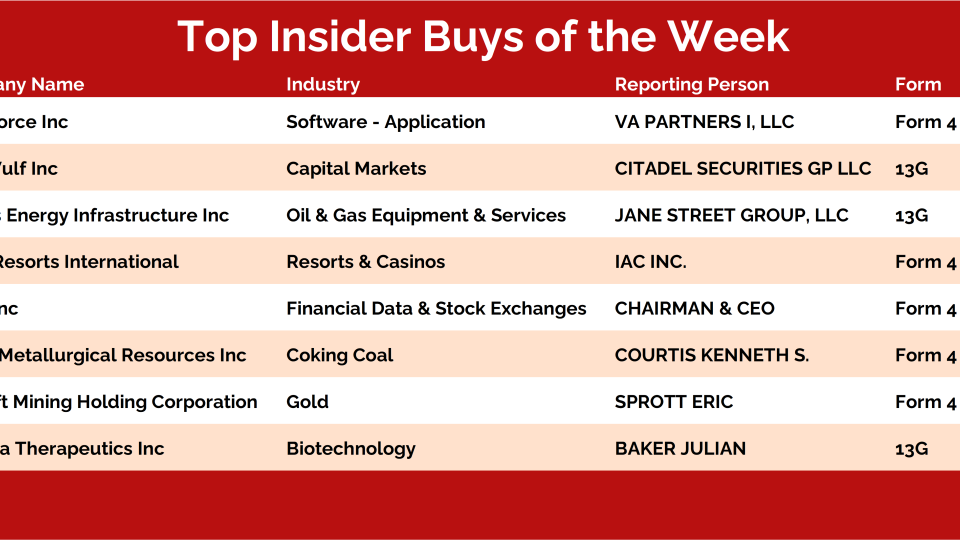

Every weekend, I dig into our insider activity tracker looking for the biggest conviction buys — and this week checked all the boxes: Baker Bros, coal stocks, big software bets, and precious metals.

The market breadth has definitely improved, but certain stocks are pushing higher on momentum, and we're here to identify just those! This week, we have a stock from the Auto sector making new highs. Let's take a look!

We retired our "Five Bull Market Barometers" in 2020 to make room for a new weekly post that's focused on the three most important charts for the week ahead.

This All Star Charts PLUS Monthly Playbook breaks down the investment universe into a series of binary decisions, tactical calls and asset allocation models.

Focusing our attention on buying stocks over the past 5-6 months has paid very well. This is especially true in the stocks that have been showing the most relative strength this year.

{kind=link}