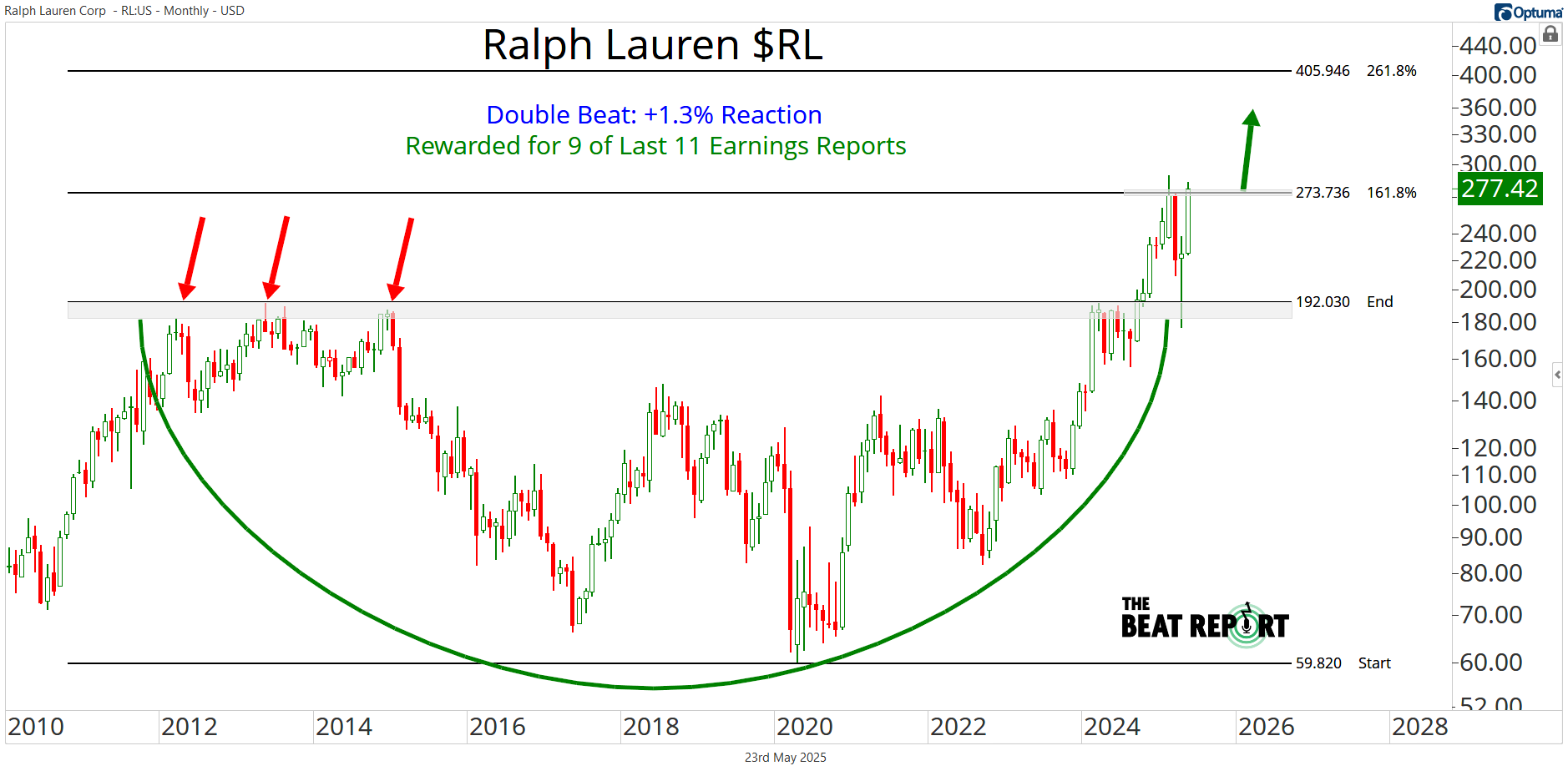

While most retail names grapple with slowing demand and shrinking margins, Ralph Lauren $RL just keeps executing.

The company delivered another double beat this quarter, marking its 9th positive reaction in the last 11 earnings reports.

That kind of consistency isn’t easy to find in this environment.

Revenue came in strong, margins held up, and the company continues to benefit from robust international demand and a premium brand strategy that’s clearly working.

This isn’t the same RL that struggled through much of the last decade.

The fundamentals have turned, and so has the market’s reaction.

The stock has resolved a massive base and is printing fresh all-time highs.

This might not be the flashiest name in Consumer Discretionary…

But it’s becoming one of the most reliable.

So what else did we learn from yesterday's earnings reactions? Let’s dive into the details.

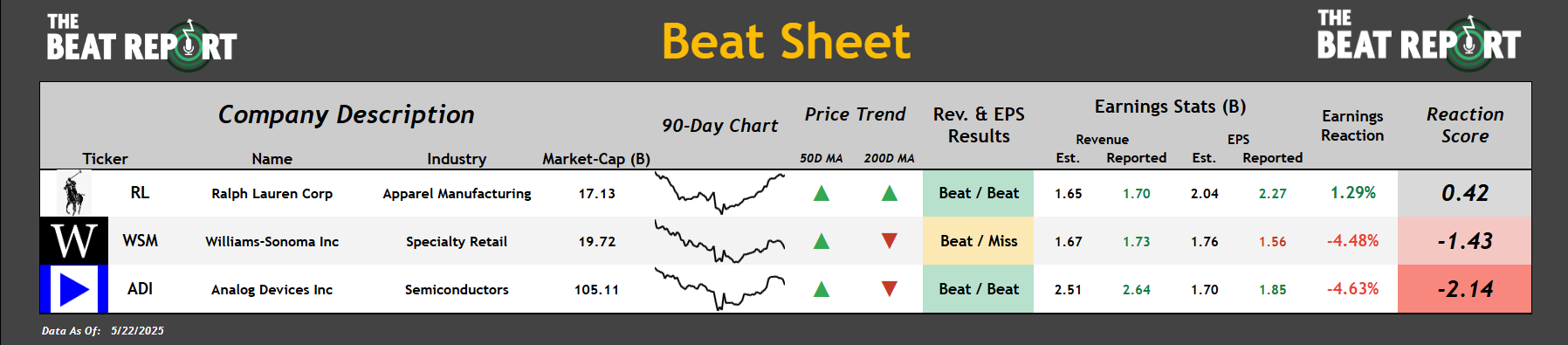

Here are the latest earnings reports from the S&P 500 👇

*Click the image to enlarge it

Ralph Lauren $RL had the best reaction score after reporting a double beat.

The company reported revenues of $1.70B, versus the expected $1.65B, and earnings per share of $2.27, versus the expected $2.04.

Analog Devices $ADI had the worst reaction score after reporting a double beat.

The company reported revenues of $2.64B, versus the $2.51B estimate, and earnings per share of $1.85, versus the $1.70 estimate.

Now let's dive into the data and talk about what happened with these reports 👇

RL has been rewarded for 9 of its last 11 earnings reports:

Ralph Lauren rallied 1.3% after this earnings report, and here's why:

All geographic regions contributed to growth: Europe led with 16% sales growth, Asia was up 13% (with China up over 20%), and North America grew 6%.

Global direct-to-consumer comparable store sales increased 13% year-over-year.

Gross margin reached 68.6%, a 200 basis point increase over the prior year.

This company is in the early innings of a brand-new growth cycle, and the market loves it.

As you can see on the chart, the price recently broke out of a multi-decade accumulation pattern.

Since then, it has soared higher to the first Fibonacci extension level. We don't think this uptrend will end here...

If RL is above 274, the path of least resistance will likely remain higher for the foreseeable future.

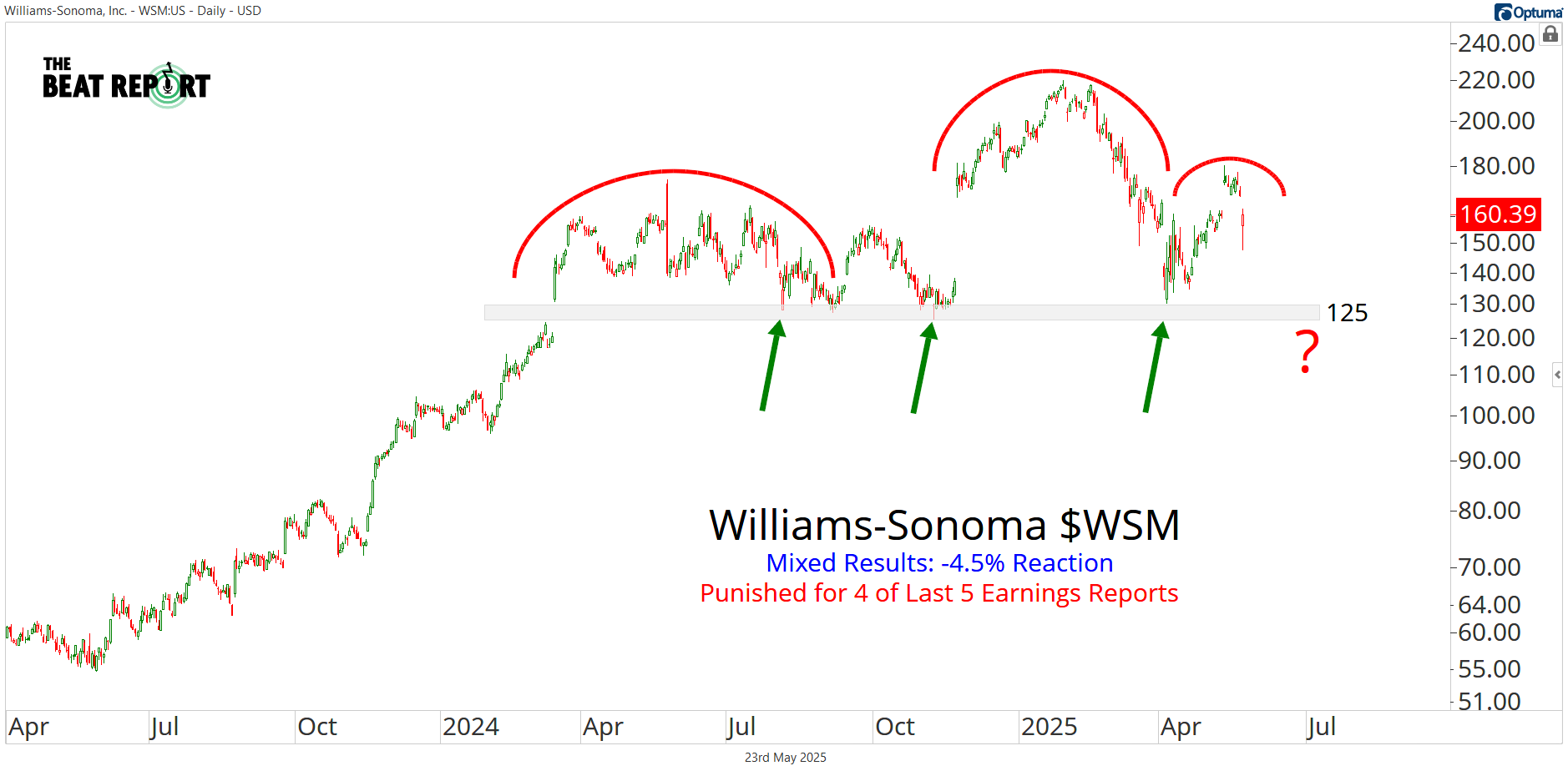

WSM has been punished for 4 of its last 5 earnings reports:

Williams-Sonoma fell 4.5% after this earnings report, and here's why:

The company’s gross margin declined by 360 basis points year-over-year.

Inventory levels increased 10.3% Y/Y due to a strategic pull-forward to mitigate tariff impacts. The market is concerned about future markdown risk if demand softens.

Management's revenue guidance for fiscal 2025 is flat to up 3% on a comparable basis, but total net revenues are expected to range from -1.5% to +1.5%

In recent years, this company has been one of the best growth stories in retail, but everything changed when Trump introduced tariffs.

The market is not interested in buying the stock. You can see this in the consistent negative earnings reactions and the textbook distribution pattern on the chart.

After a massive run-up from the spring of 2023 to early 2025, the stock has peaked and is beginning to roll over.

While the bears still have some work to do, things aren't looking good for Williams-Sonoma.

If WSM is below 125, the path of least resistance will shift from sideways to lower for the foreseeable future.

If you find our content valuable, we would greatly appreciate it if you could shareit with your friends, family, and colleagues. Your help in spreading the word is invaluable in supporting our work. Thank you to all of you who share!