One: Lululemon Reports Thursday: Athleisure on Deathwatch

I’ve been watching Lululemon literally its entire life as a public company (we covered the IPO on CNBC’s Fast Money in July of 2007). I was there from when Athleisure went from forgotten to a fad to the hottest trend in retail.

But in all that time I’ve never seen Lulu positioned quite this poorly, with a stock price and sentiment to match. The company is facing a triple crown of headwinds: Growing competition, Tariff woes, and a Fashion Revolt against the very tights that made Lulu famous (and still dominate company revenues).

Lulu reports on Thursday. I’ll have a bigger preview from Portfolio+ members. Long story short, I’m resisting the knee-jerk urge to take the other side of everything I read about retail in mainstream papers. I still think Lulu is in trouble; at this point, it’s a matter of figuring if and how to trade it.

Two: American Eagle

Tomorrow morning my whole “Denim Comeback” theory gets a big test from American Eagle Outfitters, which reports Wednesday morning. Expectations are plenty low for AEO (deservedly so, the company warns on an almost quarterly basis), but there is reason for optimism. Denim as a category is somewhere between 30 and 40% of AEO’s revenues.

Gap, Abercrombie, Walmart, and Target (among others) have all cited strength in denim as a positive. I don’t think AEO had a good second quarter, but I suspect they had a strong back-to-school period. For a company trading with nearly 30 years of technical support at ~$10/ share and 16% short interest, any optimism is likely to make for a decent reaction for bulls.

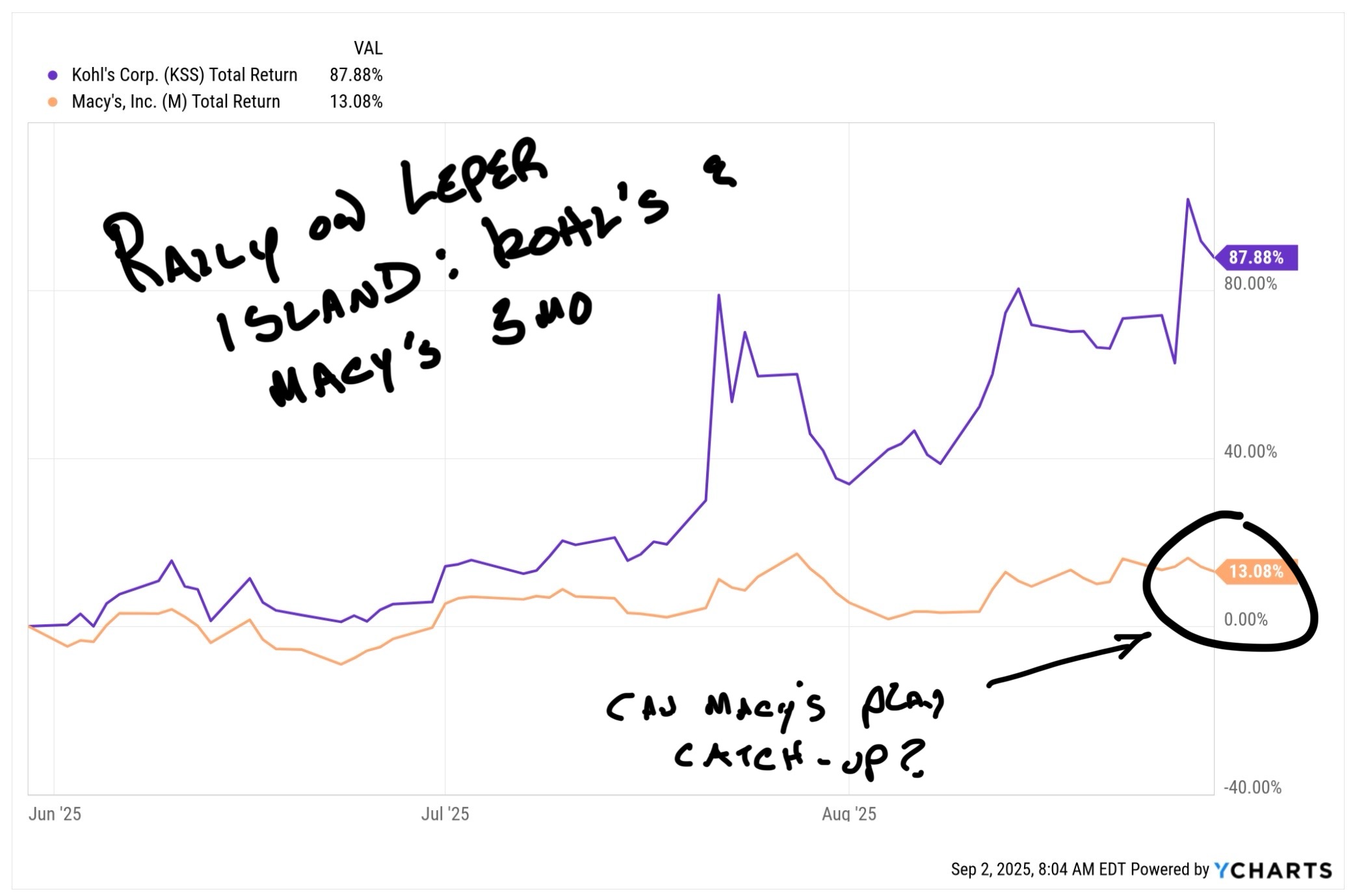

Three: Macy's

Macy’s shouldn’t really exist anymore. The last major department store standing (with all due respect to the amazing Dillard’s) has been mired with a bad business model, decades of operating the business by spending as little as possible on retail while fighting off activists and sliding into obsolescence rather gracelessly.

Macy’s results will be weak as a retailer but the value of Macy’s real estate holdings has seen a nice comeback since COVID. While less desirable locations like San Francisco have been sold off by the chain Macy’s still owns it’s NYC Herald Square store. That property alone has been valued between $4 and $9 billion since 2023.

Both Kohl’s and Macy’s have spent a lot of time and money fighting off suitors. As rates (presumably) come down and NYC office traffic finally getting back to pre-COVID levels the pressure is going to start building for Macy’s BOD to get more proactive in seeking a deal. Paradoxically bad results might be good, in this case.

Four: Tennis

Yes, tennis. It’s not about the sport as much as it’s about the fashion show and the business of athletic apparel.

The NYTimes.com covered the intersection of fashion and sport in a lengthy piece yesterday:

Despite the Times' wide-eyed wonder at this new trend, there’s nothing new here. Watching leisure sports has always been about the apparel. For more on the topic, please see: “Watching Golf is Work” from my June 13th Macke Letter.