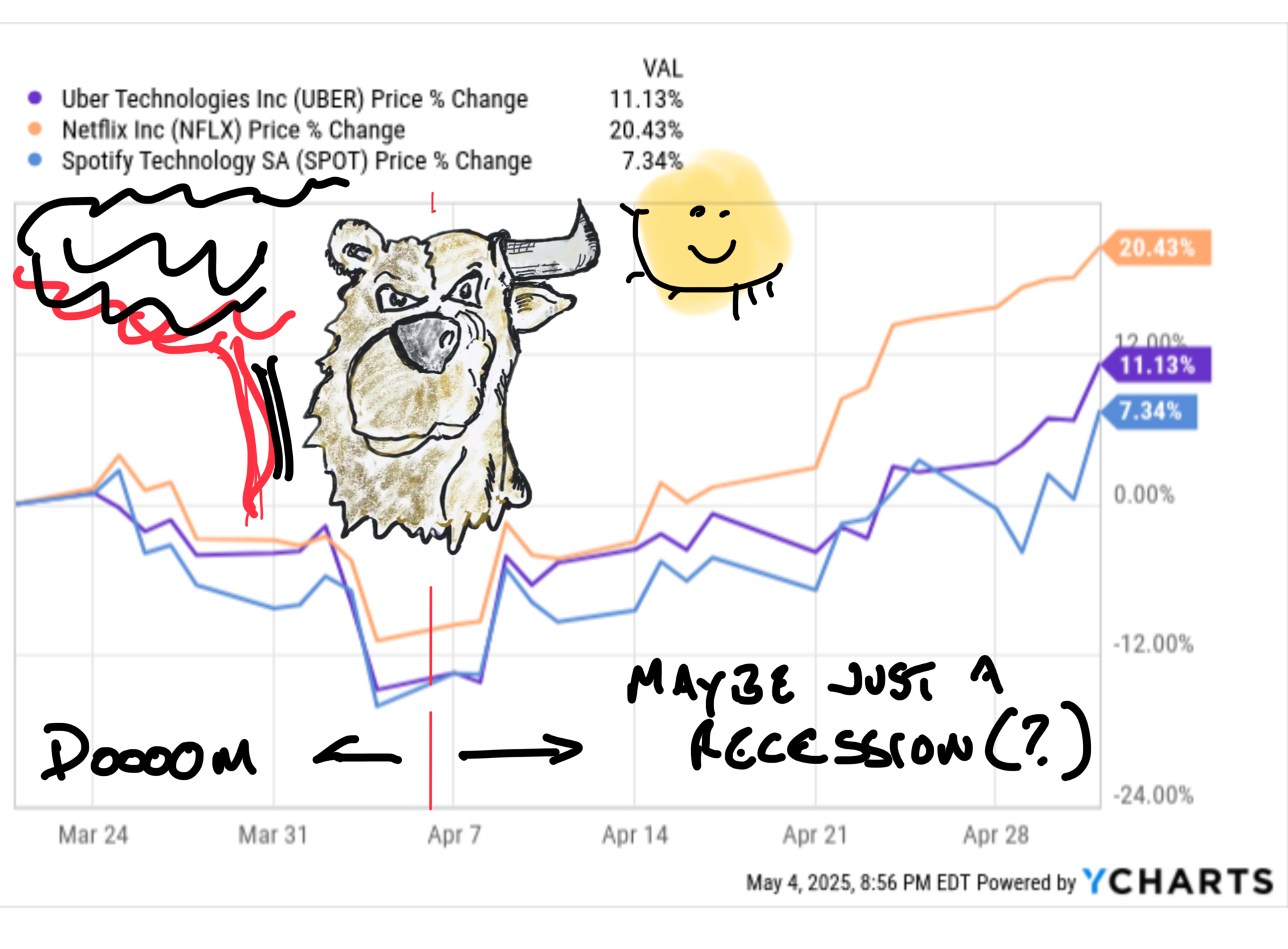

I added a new name to the Retail Round-Up portfolio last week. Spotify entered the portfolio after reporting a "disappointing" first quarter that, honestly, couldn't have made me happier.

As discussed in the Spotify preview and earnings Report Card, I didn't care much about what Spotify reported for EPS or financial guidance. I cared about subscriber count. Specifically, premium subscribers. I don't know anything more than anyone else about how these Interesting Times work out in terms of the economy over the next 6 months but I know a certain level of Chaos as been created. Whatever happens from here, everything since April 2nd has worked to the relative benefit of the most powerful, liquid, flexible consumer names.

That means Walmart, Costco and Amazon (we only own the last name in the portfolio) will take share from lesser players. It means companies like Gap and Victoria's Secret, with diversifiend supply chains and a reasonable value proposition for customers are going to pick up market share lost by companies like Kohl's and Foot Locker which are wrestling with debt and obselescence.

Economic strain means consumers arms shorten up a little. We'll still spend but we won't dig quite so deep. Based on recent COVID history it also means Americans will dig deeper into our slightly anti-social creature-comfort habits. I think Netflix, Uber and Spotify are deeply ingained into the American fabric. In an economic collapse none of the three will survive but they will be the last things the tortured American consumer releases from our cold dead hands.

I want to own all three names in my portfolio, which is why I keep talking about them. But price matters for investments. I want to buy stocks when they are getting hit by factors that don't matter to me as a long term investor.

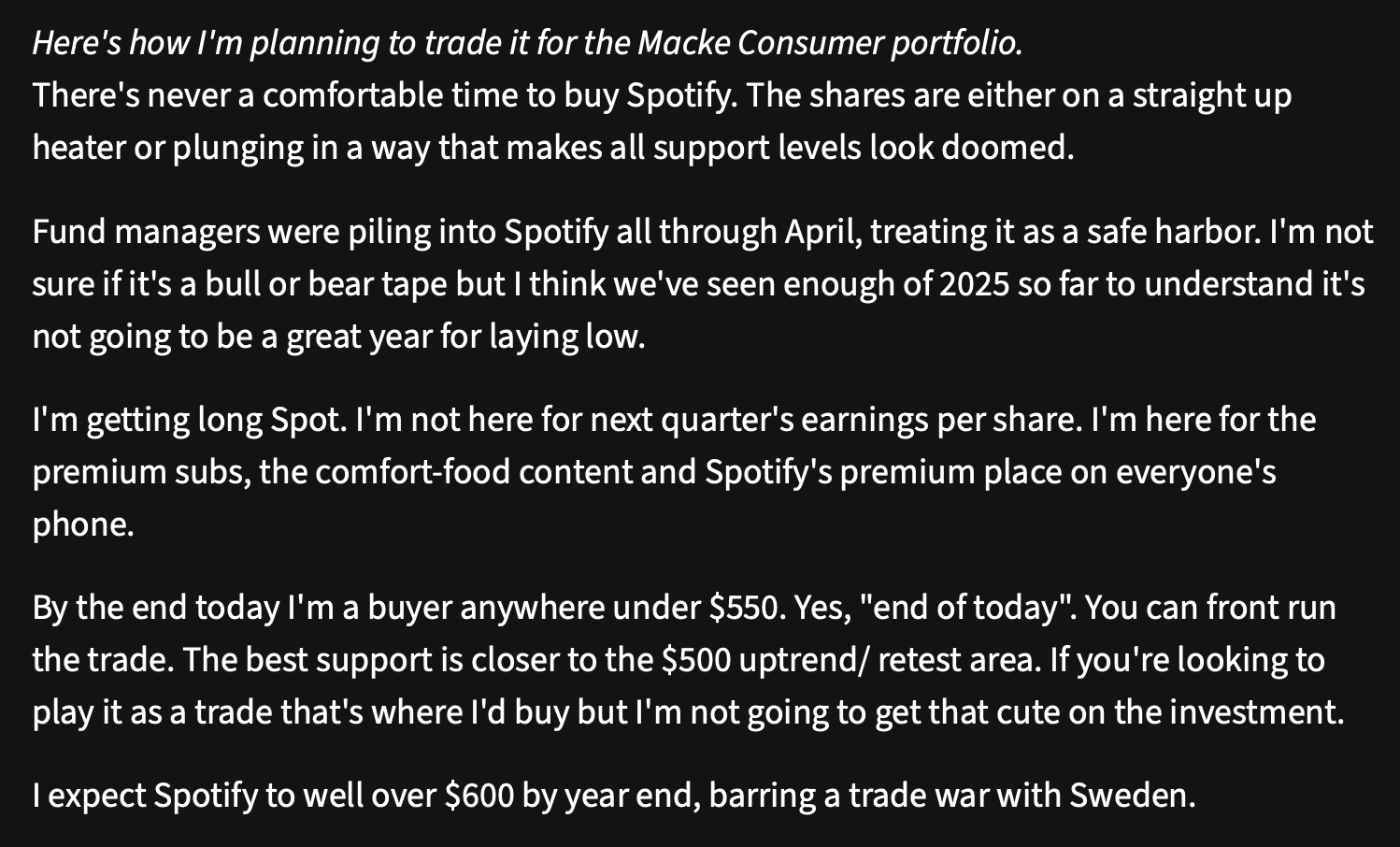

So last week when Starbucks was getting smacked to the mid-70s for doing things I want the company to do I was happy holding the shares (and explained the reasoning). That's why I didn't mind Amazon selling off on reporting pure excellence but with a "weak guide". Most importantly for our Spotify purposes, that's why I bought Spotify at $550 when shares were down 10% for missing numbers I didn't care about at all.

Getting to $500 would have been a better entry point but I'm glad I didn't wait for it. As it was there was only a few minutes where shares were below $550. I had to be quick but the price met my target and I pulled the trigger.

This week we hear from Uber on Wednesday (don't own it but would like to) and Peloton Thursday. Wildly different stories but part of the same theme. Specifically, neither is much impacted by anything less than a deep recession. Both are hard off recent lows. Uber has been running like a scalded chimp off the lows (up 30% in the last month) but has been chopping in a wide range for the last year. I'd love the chance to lock in on a pullback, ala Spotfiy.

As I finish fleshing out the portfolio I'm looking to get long but price matters. I think you can buy weakness as long as the bigger-picture, company specific story remains intact. The Bears are still noisy. The economists are outraged. Traditionally that's when you want to be out shopping. Keep your Shopping List active and updated (Nike: No longer on the list). I'll keep disecting the news and building the book.

I'll have more thoughts on Peloton Wednesday. I've got some history with the stock and the product. I'll tell you in detail what I'm watching looking for when PTON reports Thursday. Here's a hint: It isn't Q1 EPS or quarterly guidance.