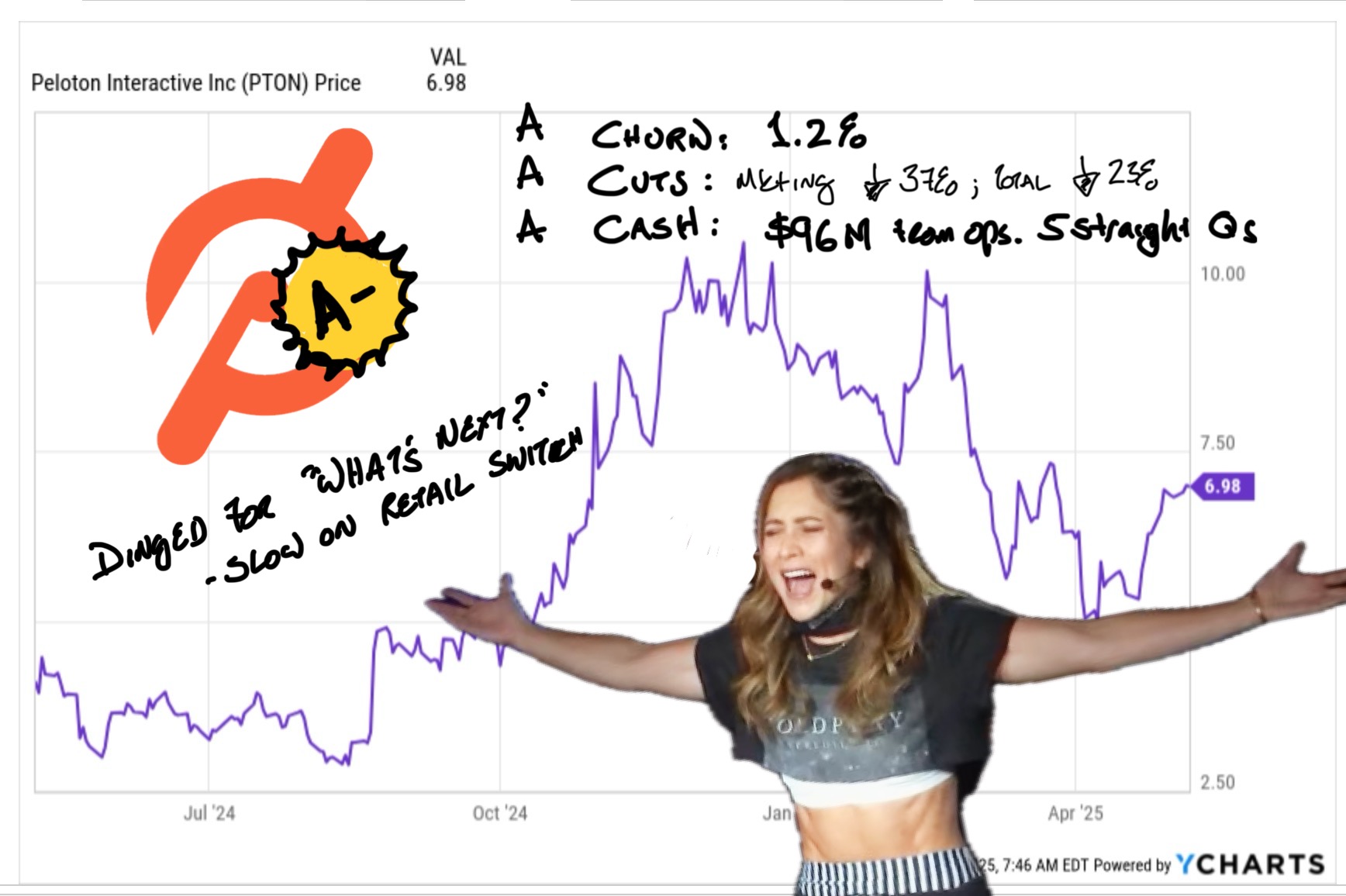

Peloton shares are down pre-market despite the company doing just about anything analysts could have asked from it.

Churn hit 1.2% despite a massive drop in marketing spend. As mentioned in the preview yesterday, if Peloton can retain the lucrative connected fitness subscribers (a decent proxy for customer satisfaction) and maintain disciplined spending you suddenly have a nice little cash flowing company with almost no built-in growth expectations.

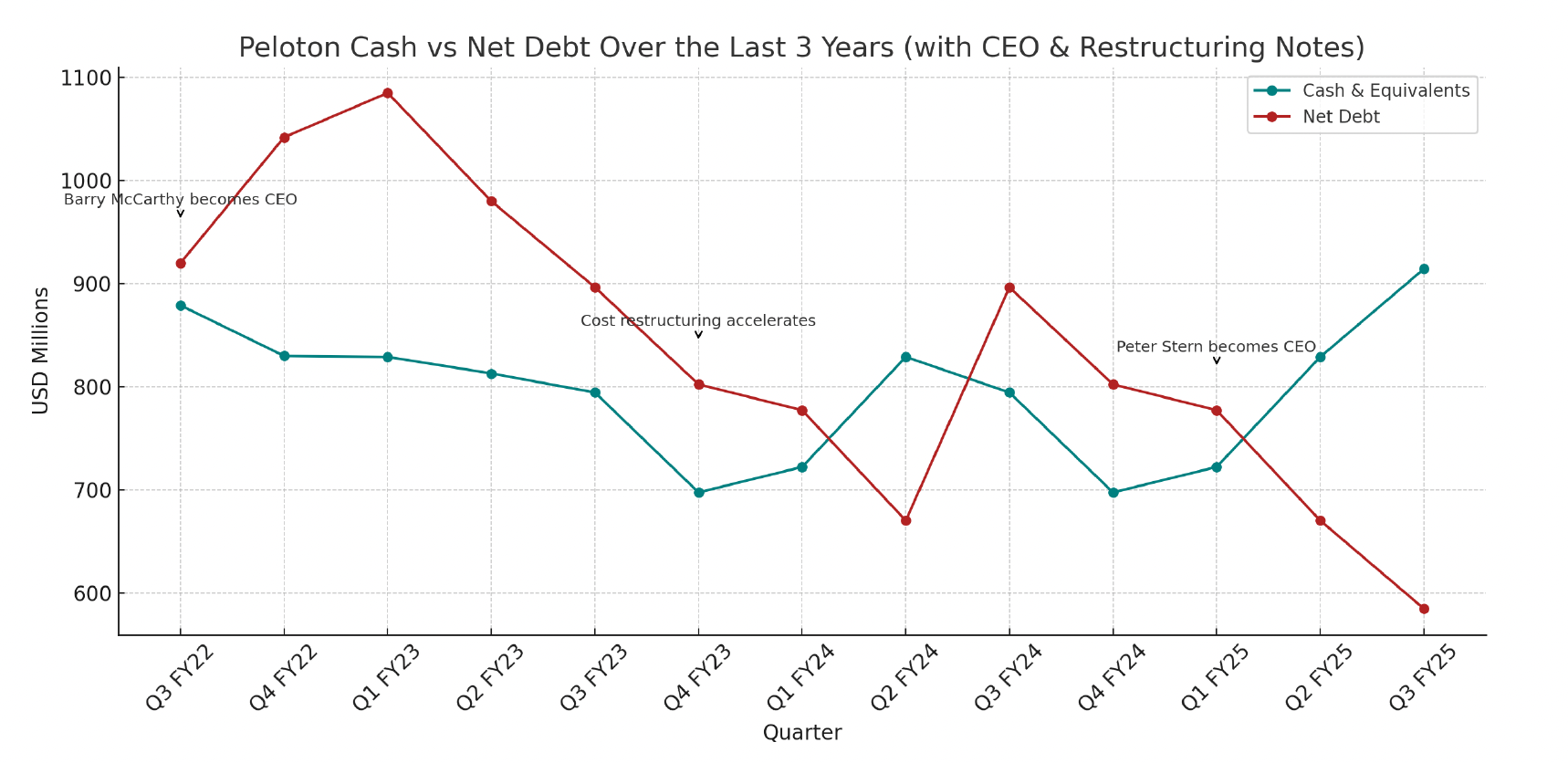

A year ago then CEO Barry McCarthy resigned with the turnaround admittedly unfinished. Barry was smart and well-meaning but he was still clinging to the idea of Peloton has a growth company. A reset was needed and that's what Peloton has gotten.

Debt is down huge over the last year, cash flow has been positive 5 quarters in a row and Peloton is finally hinting at getting out of the stores which have been driving me quietly insane for years.

The call is starting but I wanted to get a note out. Barring something very bad from the company on the call Peloton is being punished for a quarter which is, at worst, an A- (Yes, Peloton is graded much easier than, say, Amazon).